No Tax on Tips and Overtime: What Employers Need to Know

You have probably heard the headline by now.

No tax on tips.

No tax on overtime.

It sounds straightforward, but for employers, it is easy to misunderstand what actually changed.

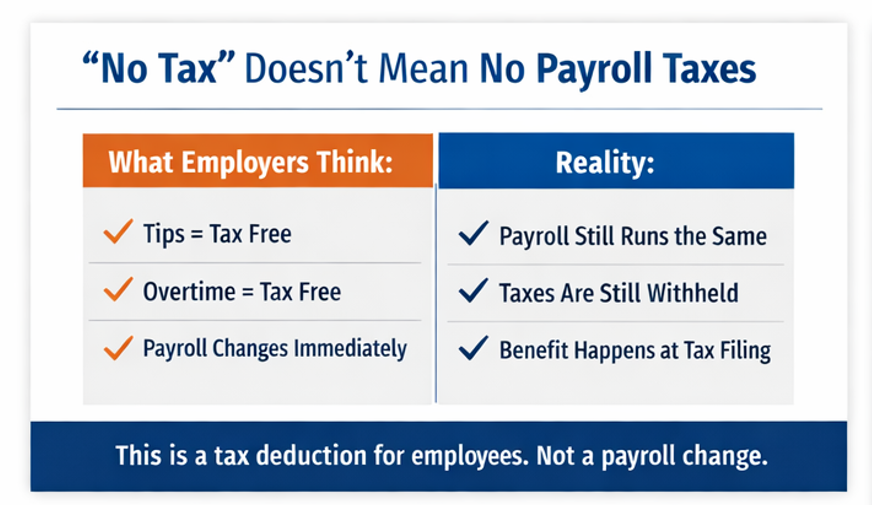

The biggest thing to know is this: these provisions created federal income tax deductions for eligible individuals. They did not eliminate an employer’s existing payroll responsibilities. For tax year 2025, the IRS says Form W-2, existing Forms 1099, Form 941, and withholding tables remain unchanged, and employers and payroll providers should continue using current procedures for reporting and withholding. CTR’s OBBBA Resource Center.

What “No Tax on Tips” and “No Tax on Overtime” Actually Mean

Under the One, Big, Beautiful Bill, eligible workers may be able to claim deductions on their federal tax returns for qualified tips and qualified overtime compensation received during tax years 2025 through 2028. The IRS says the overtime deduction is generally limited to the portion of overtime pay that exceeds the employee’s regular rate of pay, often described as the “half” portion of time-and-a-half. The deduction is available whether the taxpayer itemizes or takes the standard deduction, and both deductions phase out at higher income levels. (https://www.irs.gov/newsroom/one-big-beautiful-bill-how-to-take-advantage-of-no-tax-on-tips-and-overtime)

For qualified tips, the maximum annual deduction is $25,000. For qualified overtime, the maximum annual deduction is $12,500, or $25,000 for joint filers. In both cases, the deduction begins phasing out when modified adjusted gross income exceeds $150,000, or $300,000 for joint filers. Married taxpayers generally must file jointly to claim the deduction, and the taxpayer must have a valid Social Security number.

What This Means for Employers

For employers, the practical takeaway is simple: do not assume these provisions changed how you should run payroll in 2025.

The IRS has said employers and payroll providers should continue using current procedures for reporting and withholding for tax year 2025. That means employers should not treat tips or overtime as suddenly exempt from normal payroll processing just because employees may later qualify for a federal income tax deduction on their individual returns.

That distinction matters because employees may understandably ask why taxes are still being withheld from tips or overtime pay. The IRS has also updated its Tax Withholding Estimator to reflect these deductions, which means some employees may choose to adjust their withholding based on their own tax situation. But that is different from employers changing standard payroll treatment on their own.

What Counts as Qualified Tips

Not every amount labeled as a tip will qualify.

The IRS says qualified tips are generally voluntary cash or charged tips received from customers, including shared tips. Proposed IRS guidance also explains that the worker must be in an occupation the IRS identified as customarily and regularly receiving tips on or before December 31, 2024. The IRS occupation list includes categories such as beverage and food service, hospitality and guest services, personal services, personal appearance and wellness, recreation and instruction, and transportation and delivery.

The IRS has also clarified that some service charges do not count as qualified tips. For example, if a restaurant imposes an automatic charge for a large party and the customer cannot modify or remove it, the amounts distributed from that charge are not treated the same as voluntary tips for purposes of the deduction.

What Counts as Qualified Overtime

For overtime, the IRS says the deduction generally applies only to the portion of qualified overtime compensation that exceeds the worker’s regular rate of pay. In other words, this is generally the premium portion of overtime, not the full amount paid for those hours.

That is an important distinction for employers because this is one of the areas most likely to confuse employees. Many workers hear “no tax on overtime” and assume every dollar earned on overtime hours is fully excluded. That is not how the IRS describes the deduction.

Reporting and W-2 Considerations

For tax year 2025, the IRS says employers and other payers are not required to separately report qualified overtime compensation on Forms W-2, 1099-NEC, and 1099-MISC. Some employers may choose to separately report it in Box 14 of Form W-2 or through a separate statement or portal, but that is optional for 2025. The IRS also announced transition penalty relief for 2025 tip and overtime information reporting requirements.

The IRS has also said it is working on updated forms and guidance for tax year 2026, including changes to how tips and overtime pay are reported. On its OBBBA provisions page, the IRS says employers and other payors must report certain cash tips and the occupation of the tip recipient, and must report qualified overtime compensation on information returns, with transition relief for tax year 2025.

Because of that, employers should be reviewing whether their payroll and timekeeping processes will be able to support more detailed tracking and reporting going forward. Even if 2025 is a transition year, 2026 reporting expectations matter now.

One common mistake is assuming “no tax” means payroll tax-free treatment at the employer level. The IRS has not said that. For 2025, employers should continue current reporting and withholding procedures.

Another mistake is failing to prepare for future reporting requirements. The IRS has already said new guidance and updated forms are coming for 2026, and its current OBBBA materials make clear that tip and overtime reporting obligations still matter.

A third mistake is poor employee communication. Workers may see a headline and expect an immediate increase in take-home pay. In reality, the IRS describes these as deductions that may affect the employee’s federal return, and in some cases an employee may need to use IRS instructions or Schedule 1-A to calculate the deduction for 2025 if separate reporting is not provided.

What Employers Should Do Now

First, continue following current payroll procedures for tax year 2025 unless and until new guidance requires a change. That is the clearest direction the IRS has given employers and payroll providers.

Second, review your earning codes, timekeeping setup, and payroll reporting processes. Even with 2025 transition relief, the IRS has made clear that tip and overtime reporting requirements are part of the longer-term implementation.

Third, communicate carefully with employees. It is better to explain early that these provisions may create deductions on an individual’s federal tax return than to let employees assume their paycheck should be processed differently right now.

Fourth, keep an eye on future IRS guidance. The agency has already updated its withholding estimator, published Schedule 1-A guidance, and signaled additional reporting changes tied to 2026. Click here for the IRS guidance.

“No tax on tips” and “no tax on overtime” make for attention-grabbing headlines, but employers should be careful not to oversimplify what the law actually does.

For now, the IRS says employers and payroll providers should continue current procedures for reporting and withholding for tax year 2025. At the same time, employers should be preparing for a more detailed reporting environment as implementation continues. The real employer priority is not guessing at headlines. It is maintaining accurate payroll practices, clear documentation, and proactive employee communication.

At CTR Payroll | HR, we help employers stay ahead of changes like these with practical payroll guidance, proactive compliance support, and real-world help when the rules get complicated. Visit our OBBBA Resource Center andr Contact Us with questions!

Disclaimer: This blog is for general informational purposes and is not legal advice.

---

Since 1964, CTR has been a trusted partner. As a Payroll & HR Partner, we offer a complete Human Capital Management (HCM) solution to help businesses manage employees from hire to retire. We provide award-winning software and expert, personalized service to automate and simplify every aspect of the employee life cycle: Payroll, HR, Benefits, Workforce Management, Talent Acquisition, Talent Management, Tax, Compliance, and more.

What sets us apart? Our Dedicated Support Rep Model-your dedicated rep will know you, your business, and provide fast, expert service. Our team includes Subject Matter Experts with over 20 years of experience, ensuring you receive guidance through even the most complex situations. 📍 Based in Pittsburgh, PA, CTR is a third-generation, family-owned company with over 60 years in the business. Our core values focus on being “All In,” relentless problem-solving, and exercising the basics better than anyone-principles that have fueled our success.

If you can’t say you LOVE your Payroll & HR provider, it’s time to Contact CTR! 🌐 https://ctrhcm.com/contact 📞 Reach us: (800) 468-2794 📧 Email: sales@ctrhcm.com

View our recent HR management & compliance webinars here: https://ctrhcm.com/resources/